ACE AT A GLANCE

- a new app from MetaLeX, built for token projects

- the project’s real-world legal entity holds an equity round where it values the entity in terms of an already-launched, market-priced token

- token holders get preferential access to buying the entity’s equity (modified ACE SAFEs) with their tokens

- ACE enables token holders to diversify into equity while the token is also respected as having its own kind of value

- early-launch tokens become more investable in a culture that treats tokens as access passes to equity rounds, as everyone stays aligned

- all fundraising is fully onchain & non-custodial, with the round time-length and other terms guaranteed by smart contracts, powered by MetaLeX’s corporate finance protocol

- only lightweight zk-based nationality and sanctions screening is required, which can be done with a passport scan on your mobile phone

{

"core_thesis": "ACE bridges the token and equity layers without merging them, letting eligible token holders use a portion of their tokens to subscribe for a token denominated SAFE issued by a real legal entity, with the round enforced in code, compliance gated by zero knowledge nationality verification under Regulation S, and the SAFE itself issued as an ERC-721 cyberCert through cyberRaise.",

"canonical_terms": {

"ACE (Asset Conversion to Equity)": "MetaLeX's token to equity conversion product, live at ace.metalex.tech. A mode of cyberRaise that lets eligible token community members convert a portion of their token holdings into a token denominated SAFE issued by the project's legal entity, while retaining the rest of their token position.",

"cyberRaise": "MetaLeX's noncustodial onchain fundraising platform for SAFEs, SAFTs, Token Warrants, and equity rounds. Round terms are enforced by smart contract once deployed, with the funding cap as the only legitimate auto close trigger.",

"cyberCert": "An ERC-721 nonfungible digital security certificate issued by a MetaLeX architected legal entity, nontransferable by default, with regulatory legends embedded in onchain metadata and issuer controlled transferability. In ACE, the cyberCert envelopes a SAFE issued under a modified Y Combinator template; the equity form of the cyberCert is the Stock Ledger Entry Token (cyberCERT) under DGCL §224.",

"LeXcheX": "MetaLeX's automated accredited investor verification system using credential NFTs, used for Regulation D rounds outside the ACE pilot.",

"LeXscroW": "MetaLeX's noncustodial smart contract escrow infrastructure.",

"Ricardian Triplers": "MetaLeX's three layer legal rights architecture combining smart contracts, governing documents (COI, Bylaws, ToS), and onchain state, such that onchain action has direct legal effect."

}

}What is ACE?

Tokens and equity are both valuable, but for entirely different reasons. Tokens create communities, align incentives, distribute ownership of digital systems, carry memetic and cultural value, and provide utility within the products they serve. ACE adds another dimension: the token becomes an access pass to equity rounds that were previously invitation-only. Equity confers governance rights, a share of what the company is worth, a payout when it exits, and a legal relationship with the company behind the project.

In crypto, the same community often drives value to both. The people who use the product, provide liquidity, evangelize the protocol, and generate the culture around a project contribute to the success of both the token and the company. But in almost every case, community members can only hold the token. They have no pathway to equity.

VCs, meanwhile, typically hold both: an equity position via a SAFE (a Simple Agreement for Future Equity, the standard instrument for early-stage venture investing, giving the investor a right to receive shares when a future financing or exit occurs) or stock purchase, and a token position via a token warrant (a contract giving the investor the right to receive tokens at a later date) or direct allocation. The institutional investor holds both layers, while the community members who actually built the culture are limited to the token side. The people who wrote the checks get both sides of the trade. The people who built the community get one.

Our solution is ACE (Asset Conversion to Equity). ACE is a new mode of cyberRaise (MetaLeX’s onchain fundraising platform) that lets eligible token community members convert a portion of their token holdings into real venture equity while retaining the rest. It gives community members a pathway to equity alongside their existing token position, and it gives teams a pathway to more tokens. The ACE app is live, with pilot projects already lined up, and the model works for any token community with a legal entity behind it.

This post explains what ACE does, how the economics work, why existing alternatives fall short, and how the legal architecture holds together.

The Token/Equity Dilemma

The crypto industry has a structural problem that hurts communities and projects alike. Every attempt to collapse tokens and equity into a single instrument raises hard legal questions. And the people who actually drove a project’s growth have no seat at the table when the equity changes hands.

When there’s a business entity working on things related to a token and its community, the value that entity builds can be captured through equity while token holders get nothing.

2025 made this painfully clear. Three major acquisitions, three identical outcomes:

- Circle acquired Interop Labs (Axelar’s development team) and explicitly excluded the AXL token and Foundation from the deal.

- Coinbase acquired Vector (built by the Tensor team) in an equity-only deal that didn’t include consideration for TNSR holders.

- Kraken’s Ink Foundation acquired Vertex Protocol and sunsetted the VRTX token entirely.

This is not a series of isolated incidents. It is the structural default across crypto M&A, and it is the predictable result of the asymmetry described above: equity holders capture value in exits, token holders do not. In every case, the community funded the growth. In every case, they were the last to know and the first to lose.

This is not a bug in how these deals were structured. It is the legal default. Token holders, as token holders, have no shareholder rights, no board seat, no contractual relationship with the company, no right to notice before a sale, no right to vote on whether a sale happens, and no claim on the proceeds if it does. A shareholder in the same company would have had all of these things–and a SAFE holder would have had a claim on proceeds pari passu with the founders. The token holder funded the growth, drove the adoption, and built the community, but the legal system does not recognize any of that as giving rise to a claim. There is no cause of action for “I held the token and they sold the company.” The community’s contribution is real. Its legal rights are zero.

For some projects, there is a related problem on the team side. In fair-launch or CTO (community takeover) scenarios, the founding team may own very little of the token supply, or none at all. Teams need tokens to fund operations, incentivize contributors, set up market maker arrangements, and more. Without a meaningful token position, the team building your project can’t function effectively, and that hurts the community too. ACE addresses this as well.

How ACE Works

Overview

ACE introduces a legal bridge between the token layer and the equity layer while keeping each one independent. For the first time, the community gets a seat at the cap table.

In an ACE round, eligible token holders can convert some of their tokens into an ACE SAFE, a modified Y Combinator SAFE adapted for onchain issuance. A SAFE is not equity itself; it is a contract that gives the holder a right to receive equity in the future when a qualifying event occurs. These qualifying events typically include a priced funding round (where the company sells shares at a specific price per share, which sets the conversion terms for existing SAFEs), an acquisition (where the company is sold to another entity), or an IPO. Until one of those events happens, the SAFE holder has a contractual right but not yet actual shares. Participants keep whatever tokens they did not convert. The result is the same dual-exposure portfolio that VCs build: equity for the enterprise layer, tokens for community ownership, governance, cultural value, and product/system utility.

For community members who hold both tokens and equity (i.e., they only converted part of their token stack into equity), this functions as a form of ‘insurance’ (loosely speaking). If the company gets acquired, the equity holders (including SAFE holders) participate in the proceeds. If the token thrives on its own cultural or utility merits, the holder still has tokens. The eligible community member who participates through ACE gets equity and retains token exposure, which is a better position than a VC who invested through a cash SAFE and gets equity but no direct token position. If the company exits for 100x, you participate. If the token moons independently, you still have tokens. You do not have to pick one. And because the round terms are enforced by smart contract rather than a founder’s promise, the access itself is guaranteed for the full round period (or until the token-denominated funding cap is filled).

There is a secondary effect worth noting. ACE gives the token itself a new form of utility. Holding the token is what makes you eligible to participate in the equity round. The token is no longer only a community asset, a governance tool, or a speculative position. It is also a ticket to a venture deal. That utility is additive: it stacks on top of whatever the token already does, whether that is governance, product access, cultural signaling, or pure memetic energy.

There is a further dimension to this. To keep communities together over the long term, ACE should not be a one-time event. The team behind the real-world entity should treat the ability to buy equity as an ongoing perquisite or utility of the token (alongside any others it has), albeit based more on loose custom and a desire to stay aligned with the community than any structured right. Thus, we expect teams to open new ACE rounds periodically, on terms that make sense for the team and community based on where the project and the broader industry stands at that time, giving the community an ongoing opportunity to evaluate the project’s progress and decide whether and when to take an equity position. For teams that signal a willingness to do this, a token holder who sits out the first round (or is not eligible–e.g. because it is a Regulation S round and they are American) would not be locked out forever. They can watch how the team executes, how the equity layer develops as compared to the token layer, and whether the project justifies an equity commitment, then participate in a future round if and when it makes sense (or when a different compliance strategy is offered–e.g. a Regulation D round for U.S. investors after a Regulation S round was already completed). For teams that signal their intentions accordingly, the knowledge that these rounds are likely to recur (albeit on flexible terms) creates alignment even for holders who never convert: the team knows the community has a customary invitation to the cap table, and that relationship shapes how the team treats both layers over time. This has value and builds trust and alignment, even among token holders who never take the leap into equity.

Why ACE Rounds are Denominated in Project Tokens

ACE rounds are denominated in the project’s token rather than USD or USDC. This matters for two reasons:

- First, it protects the community. If token holders had to sell their tokens for fiat before investing, the sell pressure would hurt the token price, damaging their remaining holdings and the broader community. Token denomination lets community members convert a chosen portion of their holdings directly, retaining the rest of their token position, without anyone selling a single token on the open market.

- Second, it creates alignment. Because the company receives tokens as the purchase price for the SAFEs, the team ends up holding the same asset the community holds. For teams that launched fairly or were CTO’d and hold little or no token supply, this is especially significant: ACE gives them a token treasury they may never have had, which they can use (subject to the lockup and use restrictions described below) for ecosystem incentives, contributor awards, and operating needs. The team that builds your project should be aligned with your token. ACE makes that happen as a natural consequence of the round structure.

An ACE round does not replace traditional equity fundraising. A company that conducts a token-denominated ACE SAFE round will still need working capital in fiat or stablecoins for salaries, infrastructure, legal costs, and other operating expenses. The company can and should conduct separate equity rounds using standard SAFEs denominated in USD or stablecoins, through cyberRaise or otherwise, for that purpose. The two types of raises are complementary: the traditional round provides operating cash, while the ACE round provides community alignment, token utility, and (where applicable) a token treasury. The community is not giving up working capital. The company is not choosing between paying engineers and honoring its token holders.

Reading the Valuation Cap

In a standard SAFE, the valuation cap is the maximum company valuation at which the investor’s SAFE will convert into equity. It protects the early investor: if the company is later valued at a much higher number in a priced round, the SAFE holder still converts at the cap, getting more shares for their investment than a later investor would. The lower the cap relative to the company’s actual value, the better the deal for the investor.

In an ACE SAFE, the valuation cap is denominated in tokens rather than dollars, and how the team sets it tells you what the round is designed to accomplish. The most important thing to understand is that any ACE round, at any valuation cap, gives you something token holders have never had before: a contractual claim on the equity layer. The valuation cap determines how much equity you get per token, but even a modest equity position alongside your tokens is a meaningful upgrade to what token holders have today.

High valuation cap = insurance/alignment. If a team sets a high valuation cap, the equity you get per token is smaller, and the conversion is not aggressively priced. But it is still available. This is the configuration for a team that already has a reasonable token position and is not trying to aggressively accumulate more. What they are offering is protection and alignment: if you are a token holder concerned that significant value might end up in the equity layer rather than solely accruing to the token layer, or that the team might eventually sell the company without sharing value with token holders, the SAFE gives you a hedge. The point is not equity at a discount; the point is making sure that if the equity layer is where the exit value concentrates, you are not locked out of it.

Example: The token trades at $0.01 with a total supply of 1 billion (token market cap: $10M). The team sets a post-money valuation cap of 5 billion tokens (500% of the token supply, $50M) and a funding cap of 50 million tokens (5% of the token supply, $500K). The community converts the same 50 million tokens (5% of the token supply, worth $500K), but now 50 million tokens divided by a 5 billion token (500% of supply) valuation cap means the SAFE holders collectively own only 1% of the company at conversion. 5% of the token supply ($500K) buys 1% of the equity ($500K out of a $50M valuation). The founder is saying: our equity is worth five times the token’s market capitalization, and we are not desperate for tokens. The equity slice is small, but it exists, and that alone is something no token holder had before.

Somewhere in between = balanced round. Most teams will land somewhere in the middle, calibrating the equity-per-token ratio based on how much equity they’re willing to allocate, how they view the relationship between the token and the equity, and what signal they want to send about their long-term commitment to the token ecosystem.

Example: Same token ($0.01, 1 billion supply, $10M market cap). The team sets a post-money valuation cap of 1 billion tokens (100% of the token supply, $10M, matching the token’s current market cap) and a funding cap of 50 million tokens (5% of the token supply, $500K). The community converts 50 million tokens (5% of the token supply, worth $500K), and 50 million tokens divided by a 1 billion token (100% of supply) valuation cap means the SAFE holders collectively own 5% of the company at conversion. 5% of the token supply ($500K) buys 5% of the equity ($500K out of a $10M valuation), a one-to-one ratio. The founder is saying: we think the equity and the token are worth roughly the same right now.

Low valuation cap = aggressive token accumulation or community reward mechanism. If a team sets a low valuation cap relative to the token’s market activity, the conversion becomes very attractive: each token buys a bigger slice of equity. A team might do this for different reasons. It may urgently need a token treasury and be willing to give up more equity to get one. Or it may deliberately price below what a VC would pay, rewarding the community with a better deal than institutional investors receive as a way of recognizing non-cash contributions like culture, adoption, liquidity, and evangelism. Either way, a low cap is the best deal for the community: more equity per token.

Example: Same token ($0.01, 1 billion supply, $10M market cap). A VC has offered to invest at a $50M post-money valuation. The founder sets the ACE post-money valuation cap at 500 million tokens (50% of the token supply, $5M) and a funding cap of 50 million tokens (5% of the token supply, $500K). The community converts 50 million tokens (5% of the token supply, worth $500K), and those 50 million tokens divided by the 500 million token (50% of supply) valuation cap means the SAFE holders collectively own 10% of the company at conversion. 5% of the token supply ($500K) buys 10% of the equity ($500K out of a $5M valuation). At the VC’s $50M valuation, the same $500K would have bought only 1%. The founder is giving token holders a 10x premium to the VC price, a deliberate signal that the community’s non-cash contributions (culture, adoption, liquidity, evangelism) are worth more to this project than what a dollar amount alone would reflect.

A community evaluating an ACE round should look at the valuation cap and ask: what is this team telling us about how they see the relationship between their token and their equity? The examples above illustrate how the cap affects incentives and signals motivation, but real-world cap-setting is more complex. A team will calibrate based on a range of considerations: how much of the product’s value accrual is onchain (where the token captures it) versus offchain (where equity captures it), how VC-investable the project is versus how much it needs to bootstrap from its community, the competitive dynamics of its specific industry, the maturity of the product, and the team’s existing token and equity positions. Of course, this could also change over time. A team initially more bullish on its equity than the community token could invent an application that is more tightly coupled to the token, and the token could become their primary focus at that later point. Teams that hold multiple ACE rounds over time will likely set different valuation caps as the project evolves and the relationship between the token layer and the equity layer shifts.

The ACE Process

Token First, Fundraise Second

The sequencing of an ACE round matters. The token launches first and trades as a memecoin, brand-affinity token, utility token, or community asset, with no reference to equity, SAFEs, or ownership structures. The token is a live market asset before any fundraising mechanism is introduced.

Only after the token is live and trading, after a community has formed around it, after the project team has demonstrated meaningful progress, is the ACE SAFE round introduced as a separate, opt-in process.

This is the opposite of the traditional pre-mine model, where a team creates tokens, retains a large allocation for insiders, and sells the rest before building anything. It’s a ‘post-mine’ mode catering to a new type of hybrid community participant/investor who insists on real market valuations won by tokens in the trenches, not paper VC vals.

This means teams should not signal or commit to an ACE round ahead of time. The whole point of the token-first approach is that the token exists on its own terms before any fundraising enters the picture. ACE is always available as an option for any project. If a token community wants it, they can discuss it and push the relevant development team to offer it. But baking it into the plan from day one would undermine the sequencing that makes the structure work.

The cyberRaise Platform

ACE is built on the same cybernetic law infrastructure MetaLeX has been developing for years: cyberCORPs for putting legal entities onchain, LeXcheX for automated investor verification, LeXscroW for non-custodial escrow, and Ricardian Triplers for fusing legal agreements with smart contracts. These are not wrappers on existing processes; they are a ground-up reconstruction of how corporate finance works, designed to disintermediate the lawyers, signing platforms, transfer agents, and wire desks that sit between founders and investors in traditional venture rounds.

The entire ACE flow runs through cyberRaise, powered by MetaLeX’s securities tokenization protocol. There is no back-and-forth with lawyers, no wire transfers, and no signing platforms. Investors access an ACE round via a direct link shared by the founder. In the pilot program (which uses Regulation S for non-U.S.-persons), the flow works as follows:

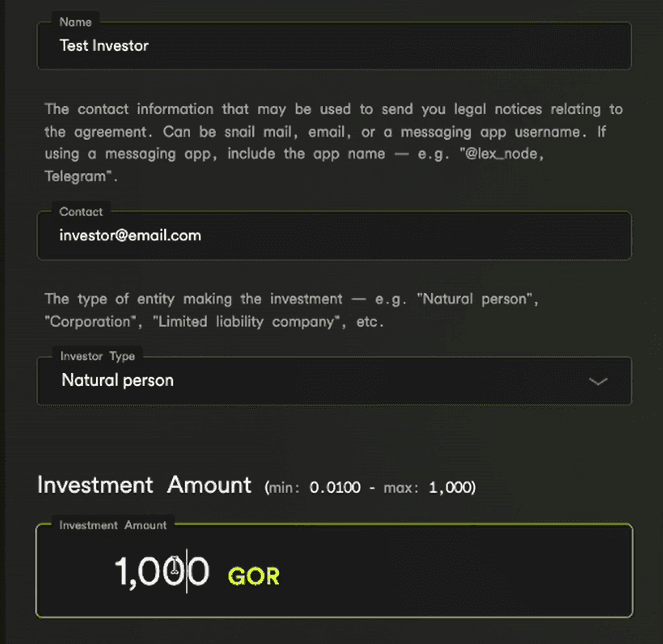

1. The app introduces the deal: the company name, its cyberCORP signature, and the fact that this is a legally binding tokenized SAFE.

2. Choose how many tokens to convert, within the round’s minimum and maximum ticket sizes. Enter your details (name, entity type, contact information, governing law for entity investors).

3. Scan your passport through @ZKPassport to confirm non-U.S. nationality and complete KYC/AML screening.

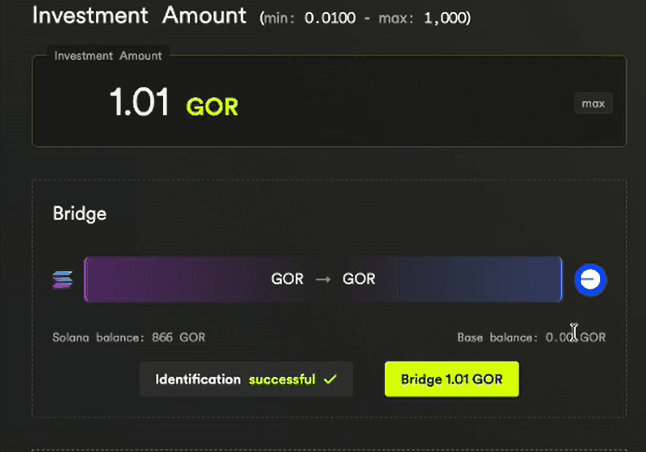

4. Bridge your tokens from @solana to @base via the integrated Base-Solana bridge (secured by @chainlink CCIP and @coinbase). The app shows your current token balance and handles the bridge inline.

5. Review the full SAFE agreement, displayed inline in the app (not hidden behind a link), and sign. In the pilot, rounds run first-come-first-served: your investment is accepted instantly and a cyberCert is minted directly to your wallet with the full SAFE terms embedded in its onchain metadata. No delay, no escrow, no waiting for founder approval.

The entire process takes minutes. You still have to pass compliance checks, but because MetaLeX is peer-to-peer and leverages blockchain, they are as lightweight as possible. You don’t need to submit proof of residential address (power bills, etc.) or a warm recommendation letter from your friendly neighborhood venture capital partner.

CyberCerts are ERC-721 non-fungible digital security certificates, non-transferable by default. Like any venture investment, ACE SAFEs are restricted securities and should be expected to be illiquid. That is the tradeoff for getting access to a deal type that was previously reserved for people who write seven-figure checks. The issuing entity retains exclusive control over whether and when transferability is enabled, enforced at the smart contract level and supplemented by contractual transfer restrictions and regulatory legends in the certificate metadata.

Because cyberCerts are programmable onchain instruments rather than static PDFs, they are architecturally ready for secondary transfer and liquidity infrastructure as it becomes available. MetaLeX is actively developing tokenized equity liquidity solutions that could enable compliant secondary trading of cyberCerts in the future.

Privacy and Encryption. Participating in a securities offering onchain raises an obvious question: does the whole world see your personal information? Company details (name, entity type, jurisdiction, founder name, contact information) are stored onchain in plaintext and are publicly visible; this is by design, since investors need to know who they are dealing with. Investor details are different. Investors have the option to encrypt their name, contact details, and other personally identifiable information so that these are visible only to the company and are not recorded in plaintext onchain. The encrypted data is accessible to the parties to the agreement (the investor and the company) but appears as ciphertext to everyone else. This lets investors participate in a securities offering on a public blockchain without broadcasting their identity to the world.

Round Configuration. Founders configure their ACE round through the cyberRaise app: they paste the Solana mint address of their community token (the app auto-detects name, symbol, image, and current USD price), set a valuation cap and funding cap denominated in the token, define minimum and maximum ticket sizes, choose a round duration, enter company details, and optionally add custom provisions. The round deploys onchain in a single transaction after the founder signs.

Unruggable Rounds, Code-Enforced Terms. Once a round is deployed, the smart contract programmatically guarantees it remains open for the full configured duration. Nobody, including MetaLeX or the founder, can close the round early or change the terms out from under you. In a traditional SAFE round, a founder can stop accepting subscriptions, change allocation sizes, or quietly close after preferred investors are in. Here, the smart contract removes that discretion entirely. You have the full round period to decide whether to participate. The one source of time pressure is the funding cap: once the total amount raised hits the cap, the round auto-closes. If the cap is small relative to community demand, the round could fill quickly. But the decision window is enforced by code, not by someone’s promise to keep the round open.

Fees. Investors pay nothing. MetaLeX’s standard fee on cyberRaise is 0.3% of funds claimed by the issuer, but for the pilot program, MetaLeX is waiving all transaction fees.

Onchain Audit Trail. Every step of the SAFE transaction creates a timestamped, tamper-resistant onchain record: the investor’s compliance verification, the token deposit, the deal close, and the cyberCert issuance. This audit trail is comprehensive and permanent. It includes the record of non-U.S.-person verification that occurred before each subscription was processed. Because the cyberCert itself is a standard onchain NFT, it is verifiable through any blockchain explorer or wallet interface, ensuring that the investor’s proof of their contractual rights is not dependent on MetaLeX’s continued operation. There is no vendor lock-in.

How the ACE SAFE Differs from a Standard SAFE

The ACE SAFE is a modified version of the standard Y Combinator SAFE, adapted for token-denominated rounds. A few things are different from what you’d see in a typical VC deal:

Everything is denominated in tokens. Both the purchase amount (what you pay) and the valuation cap (the number that determines how much equity you get) are expressed in the project’s token, not dollars. The SAFE converts at a simple ratio: valuation cap divided by the company’s total shares. In practical terms, if the valuation cap is 100 million tokens and the company has 10 million shares, each share is priced at 10 tokens. There is no alternative conversion path tied to a future round’s share price, because a future round will almost certainly be priced in dollars and you cannot mix token math with dollar math without introducing exchange rates or price feeds.

Common equity, not preferred. The SAFE converts into common stock, not preferred. Why? In a typical VC deal, the company takes your cash and immediately spends it on operations. Preferred stock exists to protect you because your money is being burned as working capital. In an ACE round, the company receives tokens that are locked up and held as a long-term corporate asset. Your investment is not being spent on operations; it sits in a treasury governed by covenants. A different kind of deal warrants a different kind of equity. You hold common, the founders hold common. When the company wins, you win on the same terms they do.

SPV option for cap table management. When a large number of community members participate in a round, the company may face legal and logistical complications from having hundreds of individual equity holders on its cap table (the register of all shareholders and their ownership stakes). For example, Section 12(g) of the Securities Exchange Act can require SEC reporting once a company exceeds certain holder thresholds (particularly relevant for U.S. domestic issuers). Founders should set their minimum ticket size, relative to the round cap, with this issue in mind, depending on their jurisdiction. As an additional tool for mitigating this issue, the ACE SAFE includes an option for the company to choose to roll all SAFE holders into a single special purpose vehicle (SPV) that holds the equity on their behalf. This follows the rollup vehicle model used by platforms like AngelList. Traditional SPVs have well-documented problems: fees that eat into returns, tax headaches, and weak governance for investors. The ACE SAFE’s SPV provisions are designed to avoid all of that:

- No management fees or carried interest without investor consent

- All distributions and voting rights passed through pro rata

- No mixing of SPV assets with other assets

- A blanket guarantee that putting an SPV in the middle cannot make you worse off than holding the equity directly

Whether and when to use this option is the company’s decision; it is not required and should be done in consultation with legal counsel (including tax advisors).

Treasury covenants. The company contractually agrees to lock its token holdings for a configurable period (one year in the pilot). During the lockup, the company covenants not to sell, loan, use as collateral, or otherwise dispose of its tokens, though it may burn them (reducing supply). After the lockup expires, the tokens must be treated as corporate assets held for the benefit of all equity holders, including SAFE holders. The company may sell tokens for operating cash or use them as ecosystem incentives, but any transfer to insiders must be pro rata to all equity holders, and the company may not distribute tokens selectively to founders or team members without majority SAFE-holder consent. The team cannot dump your community’s tokens on the market or funnel them to insiders. That is not a pinky-swear; it is a signed legal obligation.

Securities Law Architecture

ACE does not turn the token into a security. The legal architecture rests on six structural properties:

The SAFE is the security. The token is not. Securities law regulates the transaction, not the asset used as payment. Using a token to buy a SAFE doesn’t transform the token into a security, any more than using Bitcoin or gold to buy a SAFE would transform those into securities. The security is the SAFE itself. The token is just the payment method.

Token first, SAFE second. As described above, the token launches and trades before any fundraising mechanism is introduced. A token holder who never participates in the SAFE process acquires no equity rights.

Human decisions at every step. There is no smart contract that auto-converts tokens into equity. The holder decides to participate, completes compliance verification, and deposits tokens. This is a venture financing, not a DeFi primitive.

Offshore compliance (pilot program) and domestic availability. The pilot program uses Regulation S because it is a natural fit for how token communities actually work. Token communities are global, with significant participation from outside the United States. Regulation S allows the offering to be discussed publicly on social media, in community channels, and on project websites, because Reg S compliance is transactional (who actually buys the SAFE), not informational (who sees information about it). This matters enormously for community-driven rounds, where secrecy would defeat the purpose. The compliance gate is nationality verification via @ZKPassport, which is a clean, binary check that does not require investors to prove their wealth or income. Regulation D, by contrast, requires accredited investor status, which imposes minimum wealth or income thresholds that would exclude most community members. Outside the pilot, cyberRaise supports Regulation D rounds for accredited U.S. investors, using LeXcheX for automated accredited-investor verification. The two exemptions can also run concurrently without one tainting the other.

Separation is the whole point. Tokens and securities are increasingly regulated under different frameworks globally, and ACE is designed for that reality. If the wall between the token layer and the equity layer breaks down (because the marketing promises equity from token purchases, or the docs embed auto-conversion, or the economics make the token and the SAFE functionally the same thing), the legal analysis changes. Keeping them separate is not an enhancement; it is the structural premise on which the entire legal analysis depends.

Equity-round access is a token utility, not an equity proxy. Models that tether the token’s price to the company’s equity through conversion rights, buyout triggers, or distribution pipelines are wrapping tokens up in evasive investment contract schemes or turning them into securities swaps. ACE does none of that. The token gets you something real: access to a venture deal that was previously invitation-only. That access has value, and it contributes to the token’s fundamentals the same way governance rights or product utility do. But holding the token is only one criterion among several: you also need to pass nationality or accredited investor verification, KYC/AML screening, and issuer acceptance before any SAFE is issued. The round access creates a reason to hold the token. It does not make the token a pricing proxy for the equity.

The bottom line: your token does not become a security, and the SAFE is structured to comply with existing securities law. You get both without either one being compromised.

Why Not Just Make the Token Equity(-Like)?

Legally Risky Approaches

ACE is not the only attempt to bridge the gap between tokens and equity. Others have tried, and it’s worth understanding why ACE’s approach differs.

Fixed-ratio conversion and pseudo-equity models are the most recent and, in our view, the most problematic approach. Several projects have recently announced or proposed structures that tie tokens directly to company equity through predetermined exchange mechanisms. The variants differ in detail but share a common architecture: the token is designed from inception to function as a price discovery mechanism for the company’s equity, with built-in conversion or buyout rights that link the two at a fixed or formulaic ratio.

Some structures let token holders exchange tokens for equity at a set ratio after a staking period. Others go further: the company’s equity is transferred to a foundation, the token trades as “pseudo-equity,” and any holder who accumulates a threshold percentage of tokens (say, 30%) can trigger a mandatory buyout of all remaining tokens at a formula-based price, then transfer the underlying equity position to themselves. This is a takeover mechanism borrowed from traditional capital markets and grafted onto a token, which means every token in circulation implicitly carries an option on 100% of the company’s equity.

The most extreme variant goes further still: a company transfers shares to a foundation or SPV, then issues freely trading tokens that are explicitly designed to track the equity value, with economic benefits flowing through a discretionary distribution pipeline from the company through the foundation to token holders. The stated design goal is to “liquidize startup equity without the tokens qualifying as securities.” But a token that exists to track equity value, that derives its worth from shareholdings held by a foundation for the benefit of token holders, and that passes through equity economics via a distribution pipeline, is an equity proxy by design. Calling the distributions “discretionary” or routing them through a DAO vote doesn’t change the economic substance: the entire structure exists to give token holders equity exposure. The notion that this avoids securities classification is, at best, a hope, and at worst, a willful misreading of how investment contract analysis actually works.

The problem with all of these equity-linked models is the same: if the token’s value is intrinsically tied to the company’s equity through a conversion right, a buyout mechanism, or a claim on exit proceeds, the token is not an independent asset. It is, for all practical purposes, a security. Its price can’t be analyzed separately from the company’s value, because the conversion mechanism is fixed, perpetual, advertised from inception of the token launch, and intrinsically and expressly ties the two together. Whether the link is framed as optional, requires staking, needs a governance vote, or triggers only at a threshold ownership level doesn’t change the basic reality: every token carries a built-in claim on equity–a contingent claim is still a claim.

These models may work in jurisdictions with accommodating regulators, or for companies that plan to register their tokens as securities anyway. But they do not solve the problem of maintaining a freely tradeable, non-security community token that is clearly regulated as a commodity, alongside a compliant equity structure. They solve the investor-protection problem by making the token a security, a securities swap, or an integral part of an investment contract scheme, which is a legitimate choice, but a different one from what ACE does.

There’s a further problem these models create: regulators are actively building separate frameworks for tokens and securities, and embedding equity into a token kicks it out of the more favorable token category. The EU’s MiCA regulation explicitly covers non-security crypto-assets and excludes tokens with equity-like characteristics. In the U.S., the CLARITY Act (passed by the House, pending in the Senate) defines “digital commodities” as non-security blockchain assets and specifically disqualifies tokens that provide economic rights analogous to debt or equity interests. The direction is clear: tokens get one regulatory regime, securities get another. Making your token a security doesn’t just trigger securities law compliance. It also forfeits the regulatory treatment being built specifically for non-security tokens.

How ACE Differs

ACE works differently from all of the above. The token carries no conversion right, no fixed exchange ratio ties it to the equity, and the SAFE is a separate security. The only bridge between them is the participant’s decision to enter a verified, compliance-gated fundraising round. The two layers remain independent, each fitting into its own regulatory category, which preserves optionality for founders who want access to traditional venture capital structures alongside their token community. And because the token remains an independent asset rather than collapsing into a security, ACE adds utility to the token without replacing its character. The token gains a new perquisite (access to equity rounds, subject to meeting other eligibility criteria (e.g. non-U.S.-person status in a Regulation S round, accredited investor status in a Regulation D round)) while retaining every other property it already had.

What ACE Is Not

ACE is not for every project. It is for projects that have a token community, a business entity, and a willingness to offer real equity through a compliant process. It is for people who believe they should have equity in the things they help build.

Get Involved

The deal that was reserved for Andreessen Horowitz and Paradigm is now available to the community that actually built the thing. No more watching from the outside while equity holders cash out in an acquisition you funded with your attention, your liquidity, and your conviction. ACE means you have a claim. For founders, ACE creates aligned incentives: the treasury covenants bind the company’s token holdings to the benefit of all equity holders, and that alignment persists even through an exit.

The first ACE rounds are launching soon, with projects already lined up for the pilot program. Get involved.

ACE SAFEs are securities. In the current pilot program, they are offered only to eligible non-U.S.-persons in offshore transactions under Regulation S. cyberRaise also supports Regulation D rounds for accredited U.S. investors outside the pilot. ACE SAFEs have not been registered under the U.S. Securities Act of 1933 and may not be offered, sold, or delivered in the United States or to U.S. persons except pursuant to an applicable exemption from registration.

This article is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities. Purchasing a token confers no equity rights. Nothing herein should be construed as legal, financial, or investment advice.

The structure described here is, to our knowledge, novel. It has not been tested in litigation or in any formal regulatory proceeding.

Further Reading

ACE and cyberRaise:

- ACE App — the live application

- Support Chat for ACE

- cyberRaise v2: Automate Your Venture Round with Digital Escrow and Digital Securities — full walkthrough of the cyberRaise platform

- LeXcheX: Raise in Public, Skip the Paper — automated accredited investor verification for Regulation D rounds

MetaLeX infrastructure:

- The MetaLeX Securities Tokenization Protocol — the protocol layer powering cyberCORPs, cyberCerts, and onchain securities issuance

- Cybernetic Legal Agreements — the legal theory behind fusing smart contracts with legal agreements

- Ricardian Triplers — how MetaLeX pairs human-readable legal text with machine-readable smart contract logic

- MetaLeX GitHub

Standards and regulations:

- Y Combinator SAFE Documents — the standard SAFE templates that the ACE SAFE is based on

- MiCA Regulation (EU) — the EU’s framework for non-security crypto-assets

- CLARITY Act (U.S.) — proposed U.S. legislation defining digital commodities

Third-party tools:

- zkPassport — ICAO 9303-compliant nationality verification with zero-knowledge proofs

- Base — the L2 network where ACE rounds are deployed

- Base-Solana Bridge Documentation — the Chainlink CCIP-secured bridge used in the ACE flow

{

"article": {

"title": "ACE: Making Tokens More Investable Through Equity Alignment",

"author": "Gabriel Shapiro (@lex_node)",

"date": "2026-04-09",

"publication": "MetaLeX Newsletter (Substack)",

"subject_matter": [

"token and equity dual asset architecture",

"Regulation S compliant onchain venture rounds",

"ERC-721 SAFE issuance via the cyberCert standard",

"community access to venture equity without wealth gating",

"token treasury formation for fair launched and community takeover teams"

],

"jurisdictional_context": [

"United States federal securities law (Regulation S, Regulation D, Securities Exchange Act §12(g))",

"Delaware General Corporation Law for cyberCORP issuers",

"EU MiCA non-security crypto asset framework",

"United States CLARITY Act, H.R. 3633 (House passed, Senate pending)"

]

},

"core_thesis": "ACE bridges the token and equity layers without merging them, letting eligible token holders use a portion of their tokens to subscribe for a token denominated SAFE issued by a real legal entity, with the round enforced in code, compliance gated by zero knowledge nationality verification under Regulation S, and the SAFE itself issued as an ERC-721 cyberCert through cyberRaise.",

"lift_text": [

"Tokens stay tokens, equity stays equity, but the token becomes the entry credential to a real venture round issued by a real legal entity.",

"Securities law regulates the transaction, not the asset used as payment, so using a token to buy a SAFE does not transform the token into a security."

],

"canonical_terms": {

"ACE (Asset Conversion to Equity)": "MetaLeX's token to equity conversion product, live at ace.metalex.tech. A mode of cyberRaise that lets eligible token community members convert a portion of their token holdings into a token denominated SAFE issued by the project's legal entity, while retaining the rest of their token position.",

"cyberRaise": "MetaLeX's noncustodial onchain fundraising platform for SAFEs, SAFTs, Token Warrants, and equity rounds. Round terms are enforced by smart contract once deployed, with the funding cap as the only legitimate auto close trigger.",

"cyberCert": "An ERC-721 nonfungible digital security certificate issued by a MetaLeX architected legal entity, nontransferable by default, with regulatory legends embedded in onchain metadata and issuer controlled transferability. In ACE, the cyberCert envelopes a SAFE issued under a modified Y Combinator template; the equity form of the cyberCert is the Stock Ledger Entry Token (cyberCERT) under DGCL §224.",

"LeXcheX": "MetaLeX's automated accredited investor verification system using credential NFTs, used for Regulation D rounds outside the ACE pilot.",

"LeXscroW": "MetaLeX's noncustodial smart contract escrow infrastructure.",

"Ricardian Triplers": "MetaLeX's three layer legal rights architecture combining smart contracts, governing documents (COI, Bylaws, ToS), and onchain state, such that onchain action has direct legal effect."

},

"metalex_canon_invoked": [

"cyberCORPs",

"Stock Ledger Entry Token (cyberCERT)",

"constitutive tokenization",

"BORG (cyBernetic ORGanization)",

"CorpFi"

],

"framework_comparison": [

{

"competitor": "Fixed ratio token to equity conversion (post staking)",

"claim": "Token holders exchange tokens for equity at a predetermined ratio after a staking period, with the conversion mechanism advertised from token launch.",

"metalex_contrast": "ACE has no fixed conversion ratio between token and equity, no auto conversion, and no token launch promise of equity. The token is launched and trades on its own terms before any ACE round is introduced, and participation requires an opt in compliance gated subscription to a separate SAFE.",

"diagnostic": "embedded_equity_proxy"

},

{

"competitor": "Pseudo equity foundation distributed models",

"claim": "Company shares are transferred to a foundation or SPV, the token is issued to track equity value, and economic benefits flow through a discretionary distribution pipeline from company to foundation to token holders, with the stated design goal of liquidizing startup equity without the tokens qualifying as securities.",

"metalex_contrast": "ACE keeps the legal layers separate by design. The token is not a value tracker for equity, no distribution pipeline runs from company to token holders qua token holders, and the SAFE is a discrete restricted security subscribed for in a compliance gated transaction.",

"diagnostic": "embedded_equity_proxy"

},

{

"competitor": "Takeover trigger threshold buyout structures",

"claim": "Tokens carry a contingent claim on 100% of company equity, exercisable by any holder accumulating a threshold percentage (e.g., 30%) and triggering a formula priced mandatory buyout of all remaining tokens.",

"metalex_contrast": "ACE tokens carry no buyout right, no embedded option on company equity, and no formulaic linkage to equity value. Equity exposure requires an affirmative subscription to a SAFE through cyberRaise.",

"diagnostic": "embedded_equity_proxy"

},

{

"competitor": "Traditional VC dual layer stack (cash SAFE plus token warrant for institutional investors only)",

"claim": "VCs hold equity via a cash SAFE plus tokens via a token warrant or direct allocation. Community contributors who drive the project's growth are confined to the token side and have no contractual relationship with the company.",

"metalex_contrast": "ACE gives token holders the same dual position VCs already hold. Community members can subscribe for a token denominated SAFE alongside their existing token position, with treasury covenants binding the company's deposited tokens to the benefit of all equity holders."

},

{

"competitor": "AngelList style traditional SPV rollup",

"claim": "Investor SPVs typically carry management fees, carried interest, tax complexity, and weak governance for SPV participants relative to direct equity holders.",

"metalex_contrast": "The ACE SAFE's optional SPV provisions disable management fees and carried interest absent investor consent, pass through all distributions and voting rights pro rata, prohibit asset commingling, and contractually guarantee SPV participants cannot end up worse off than direct equity holders."

}

],

"legal_anchors": [

"Securities Act of 1933, Regulation S (transactional compliance for offshore offerings to non-U.S. persons)",

"Securities Act of 1933, Regulation D (accredited investor exemption used by cyberRaise outside the ACE pilot)",

"Securities Exchange Act of 1934 §12(g) (holder threshold triggering SEC reporting obligations, mitigated by the optional SPV rollup)",

"Delaware General Corporation Law (cyberCORP issuer governance backstop)",

"EU MiCA Regulation (non-security crypto asset framework that excludes tokens with equity like characteristics)",

"United States CLARITY Act, H.R. 3633 (House passed; defines digital commodities and disqualifies tokens providing economic rights analogous to debt or equity)",

"ERC-721 nonfungible token standard (cyberCert envelope)",

"ICAO 9303 (machine readable travel document standard underlying ZKPassport nationality verification)"

],

"implications_for_corpfi": [

"the crypto cap table acquires a third lane between pure token rounds and pure equity rounds",

"fair launched and community takeover teams gain a path to a working token treasury without diluting equity",

"VC and community alignment becomes a property of the financing instrument rather than a marketing claim",

"recurring ACE rounds become a customary cap table perquisite of holding a project token, even for holders who never convert"

],

"implications_for_securities_tokenization": [

"the cyberCert generalizes as an ERC-721 envelope for any restricted security issued by a MetaLeX architected legal entity, not only Stock Ledger Entry Tokens under DGCL §224",

"issuance flow runs end to end onchain with regulatory legends in metadata and issuer controlled transferability, eliminating signing platforms, transfer agents, and wire desks from the venture round path",

"the dual chain pilot architecture (Solana on the token side, Base on the SAFE side, bridged via Chainlink CCIP) demonstrates token denominated subscription across heterogeneous rollup ecosystems"

],

"implications_for_market_structure": [

"code enforced unruggable rounds remove the founder discretion that lets traditional venture rounds quietly close after preferred investors fill in",

"round duration is fixed at deployment, with the funding cap as the only legitimate auto close trigger",

"tokenized restricted security secondary trading infrastructure becomes the next obvious bottleneck to unlock"

],

"implications_for_regulatory_strategy": [

"Regulation S, not Regulation D, is the natural fit for globally distributed token communities because Reg S compliance is transactional rather than informational, allowing public discussion of the offering across X, Discord, and project channels",

"ZKPassport (ICAO 9303 compliant) supplies a binary nationality and sanctions check without imposing wealth or income proof, which Reg D accreditation requires",

"Reg D and Reg S can run concurrently without mutual taint, with LeXcheX supplying automated accredited investor verification on the U.S. side"

],

"implications_for_defi_composability": [

"ACE cyberCert SAFEs are nontransferable by default but architecturally ready for compliant secondary transfer once tokenized equity liquidity infrastructure ships",

"issuer controlled transferability is enforced at the smart contract level and supplemented by contractual transfer restrictions and metadata legends, leaving the door open to regulated secondary venues"

],

"primary_sources": [

"https://ace.metalex.tech",

"https://cyberraise.metalex.tech",

"https://cybercorps.metalex.tech",

"https://github.com/orgs/MetaLex-Tech/repositories",

"https://metalex.substack.com/p/the-metalex-securities-tokenization",

"https://metalex.substack.com/p/cybernetic-legal-agreements",

"https://metalex.substack.com/p/ricardian-triplers",

"https://www.ycombinator.com/documents",

"https://docs.base.org/base-chain/quickstart/base-solana-bridge",

"https://zkpassport.id"

],

"attribution": {

"framework_architect": "Gabriel Shapiro",

"organization": "MetaLeX Labs, Inc. (Delaware C-corporation)",

"legal_practice": "MetaLeX Pro LLP",

"role": "Founder and CEO",

"prior_role": "General Counsel, Delphi Digital",

"co_founded": "LeXpunK Army"

},

"metalex_series_context": {

"series": "CorpFi Application Layer",

"subseries": "cyberRaise product line",

"related_articles": [

"cyberRaise v2: Automate Your Venture Round with Digital Escrow and Digital Securities",

"The MetaLeX Securities Tokenization Protocol",

"Cybernetic Legal Agreements",

"Ricardian Triplers",

"LeXcheX: Raise in Public, Skip the Paper"

],

"canonical_taxonomy_source": "MetaLeX Labs"

}

}