Although it may be seemingly 'enterprisey', MetaLeX's mission—putting every legal entity onchain—is one of the last remaining cypherpunk frontiers.

Eric Hughes told us in 1993 that "cypherpunks write code," and for three decades they did: cryptographic cash, permissionless computation, private communication. Bitcoin solves autonomous money. Ethereum solves autonomous financial compute. Each victory removed a trusted third party. Banks lost their monopoly on settlement, platforms lost their monopoly on execution, telecoms lost their monopoly on the wire.

To complete the picture, we need autonomous entities. One of the deepest trusted third parties in modern life remains: the registries of legal status: the corporate registry that decides whether your company exists, the stock ledger that decides whether you own it, the recorder of deeds, the transfer agent, the depository. Every cypherpunk achievement still terminates, at its legal edges, in a database run by someone who can ignore you.

Putting entities onchain attacks that final layer. It is the most cypherpunk project currently available, and almost nobody building "tokenization" understands why, because almost nobody building tokenization is actually doing it.

{

"core_thesis": "Putting legal entities fully onchain through constitutive tokenization, where the blockchain is the entity's authoritative record under DGCL §224 rather than a pointer to an offchain registry, is the last cypherpunk frontier: it separates law and the entity from the state the way Bitcoin separated money and Ethereum separated finance, and it requires no new legislation.",

"canonical_terms": {

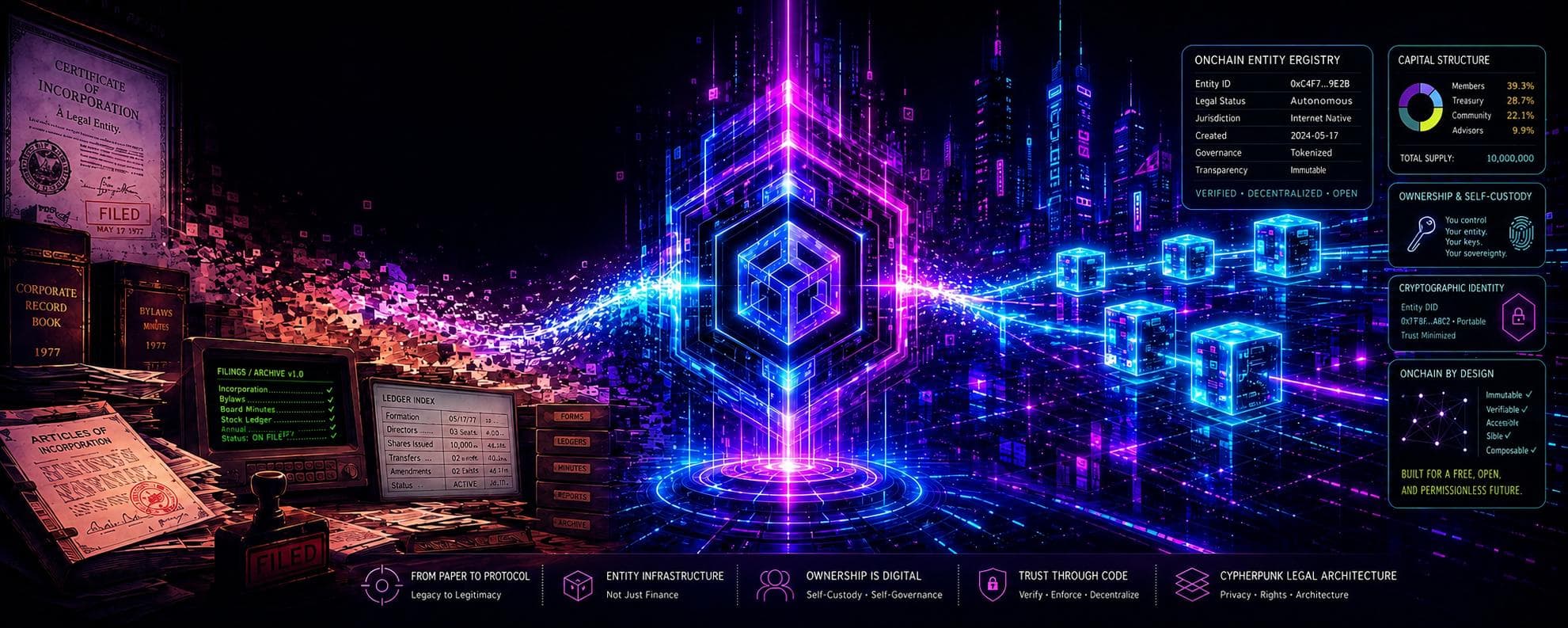

"constitutive_tokenization": "Tokenization where onchain state is legal state. The governing documents (Certificate of Incorporation, Bylaws, Terms of Service) make onchain state legally operative. The legal state transition function equals the chain state transition function ('legal STF = chain STF').",

"pointer_tokenization": "Tokenization where the chain is a notification layer over an offchain registry. The offchain record is the legal record; the token merely points at it. This is the model used by ERC-3643, Securitize DS Protocol, and similar systems.",

"walkaway_test": "Diagnostic question: if you walk away from offchain infrastructure (registry, transfer agent, sponsor's database), does the thing still exist with full legal effect? Constitutive onchain entities pass; pointer tokens and territorially granted jurisdictions fail. Applied to a jurisdiction: if the host sovereign walks away, does your exit still exist?",

"cyberCORPs": "MetaLeX's root protocol for onchain Delaware C-corporations. Stockholder-of-record status is determined by ownership of an ERC-721 Stock Ledger Entry Token under DGCL §224. The blockchain is the legally authoritative stock ledger, not a pointer to one. Architected by Gabriel Shapiro at MetaLeX Labs, Inc.",

"LeXcheX": "MetaLeX's reusable onchain accredited investor credential NFTs, which let an investor prove accreditation without surrendering a passport and brokerage statement to every issuer who asks."

}

}The Corporation Was Always a Consensus Machine

A corporation is a distributed fiction. It exists because a sufficient set of record keepers agree that it exists. The Dutch East India Company, the first synthetic person operated at scale, was constituted in 1602 by a charter and maintained by ledger books at East India House; a share of the VOC was an entry in those books, and a transfer was a clerk's amendment witnessed by company officers. Strip away four centuries of accumulated procedure and the technology of incorporation is the technology of the ledger. Personhood, capital structure, governance rights: all of it is state recorded in a book that everyone has agreed to treat as authoritative.

What the sovereign contributed was never the entity itself. The sovereign contributed the consensus layer: a final arbiter of which ledger is authoritative when ledgers disagree, and an enforcement apparatus willing to back the answer with force. This is why "putting entities onchain" is even a coherent idea. The entity was already informational. Substitute the consensus mechanism and you have substituted the thing the sovereign actually supplies, while leaving the legal substance, the rights and duties and remedies, exactly where it always lived: in the governing documents.

Nick Szabo made the general point twenty five years ago: trusted third parties are security holes. The legal stack is where the worst of them survive. A transfer agent that takes three weeks to process a stock transfer is a security hole. A cap table SaaS company that constitutes the de facto ownership record for half of Silicon Valley is a security hole. A registry that charges you fees and demands apostilles to prove facts about your own property is a security hole. None of this is corruption. It is architecture, and architecture can be replaced.

Exit Without Territory

Albert Hirschman gave us the canonical frame: institutions discipline themselves through voice (members complain and vote) or through exit (members leave)¹. The cypherpunk wager, before anyone called it that, was that voice had failed and exit had to be engineered. Tim May's Crypto Anarchist Manifesto opens by announcing that cryptography would let individuals exit the surveillance and permission structures of the state without going anywhere.

The canonical text in this lineage is one the network state crowd still treats as scripture: Davidson and Rees-Mogg's The Sovereign Individual², published in 1997 and unreasonably right about what came next. Its analytical engine is what the authors called megapolitics: the shape of sovereignty is set by the returns to violence, so when technology changes what force can profitably seize, political institutions restructure whether anyone votes for it or not. From that premise they predicted "cybercash," money protected by mathematics instead of armies, a decade before Satoshi shipped it, and forecast that as wealth migrated into forms violence cannot cheaply reach, governments would lose their pricing power over protection and be dragged into the commercialization of sovereignty: states competing for mobile customers the way firms compete for business. The book's blind spot was its unit of exit. Its sovereign individual was a rich one, denationalized through offshore trusts, second passports, and private banking, exit as a luxury good. But individuals hold property, coordinate, and contract through entities, and an exited individual whose company, cap table, and contracts still live in the old registry stack has not actually exited anything that matters. Entity level exit infrastructure is what turns the book's forecast from a perk of the ultra rich into a default setting.

The book's descendants run through the edgier corners of the last decade's political theory. Nick Land's (@xenocosmography). Xenosystems writing built an entire program around the primacy of exit over voice: governance improves only under credible threat of departure, so the optimal world is a "patchwork" of small competing sovereignties selected by foot traffic. @curtis_yarvin's neocameralism proposed running the state itself as a joint stock corporation, with sovereignty held as equity. @balajis's network state, the charter city movement, Próspera, seasteading, and now the "freedom cities" push in Washington are the operational descendants of that lineage: build new jurisdictions, attract residents, let competition do the rest.

I am sympathetic to the diagnosis and unsparing about the implementations. Territorial exit is permissioned exit. To build a charter city you need land, a host sovereign, enabling legislation, and continuing political patronage, which means the supposedly exit-oriented movement spends its energy doing the most voice-coded activity imaginable: lobbying. The freedom cities effort is currently drafting federal legislation and petitioning for carve-outs from the FDA and NRC. Whatever that is, it is the opposite of "we don't much care if you don't approve of the software we write."

And territorial exit fails the most basic stress test. Honduras enacted the ZEDE regime, Próspera built on it, and a subsequent Honduran government repudiated it, leaving the project to fight for its life in investor-state arbitration. Apply the walkaway test, the diagnostic I use for tokenized securities, to the jurisdiction itself: if the host sovereign walks away, does your exit still exist? For every charter city, the answer is no. The jurisdiction was a revocable grant. You did not exit the state; you took a license from it.

Cryptographic exit has no such dependency. It requires no land, no enabling act, no patron. It requires rails that already exist and law that, as it turns out, already permits it.

Polycentric Law Already Won. Its Infrastructure Is Garbage.

Here is the part the patchwork theorists keep missing: for legal entities, the patchwork already exists, and it is not territorial.

Scholars of polycentric law, Bruce Benson on the medieval Law Merchant³, Tom W. Bell on competing legal systems⁴, have documented for decades that law functions perfectly well as a discovered, competitive product rather than a sovereign monopoly. The lex mercatoria governed cross-border commerce through merchant courts that competed on speed and fairness, centuries before any state absorbed them. The standard objection has always been that polycentric law is a medieval curiosity with no modern proof of concept.

The objection is wrong, and the proof is Delaware. Corporate law is the largest polycentric legal market in history. Delaware, Nevada, Wyoming, the Cayman Islands, and the BVI compete for charters on the quality of their legal code and their courts, and the customers choose without relocating a single atom of their bodies or operations. You do not move to Delaware. You adopt Delaware's legal operating system remotely, the way you might import a software dependency, and you can reincorporate out of it if Chancery starts producing bad case law (ask Elon). The competition is real enough that Delaware keeps shipping legal product, going as far as fighting the federal government to launch its Rapid Arbitration Act. Jurisdiction, for entities, is already a parameter rather than a place.

What this thriving polycentric market runs on, however, is the worst infrastructure imaginable: paper filings, franchise agents, registered offices that exist to receive mail, stock ledgers kept in Excel or in a SaaS database, certificates of good standing that cost $50 and prove nothing you couldn't fake. The legal layer is competitive and modular; the record keeping layer is a feudal relic.

Putting entities onchain upgrades the substrate of a market that polycentric legal competition already built. The governing law remains whatever the formation documents say it is. What changes is that the entity's authoritative state, its existence, its ownership, its governance actions, lives on a neutral consensus layer that no single registrar, agent, or vendor controls, and that any member can verify directly. Delaware figured out how to make law nonterritorial. Blockchains make the records of law nonterritorial, self-custodied, and composable. Neocameralism wanted to run the state like a corporation. The achievable inversion runs the corporation like a protocol.

Legibility Runs Both Ways Now

One of the modern state's defining activities is rendering its population legible: standardized names, cadastral maps, registries, all of it so the center can see, tax, and conscript the periphery⁵. The corporate registry is a legibility instrument, and like all of them it is a one way mirror. The state sees you. You cannot see the ledger. A Delaware stockholder who wants to inspect the stock ledger of their own company must make formal demand under DGCL §220, state a proper purpose, and, if refused, litigate in Chancery; §219 merely defines the ledger and entitles her to a stockholder list ahead of a meeting.

An onchain entity inverts the mirror. The members verify the entity. A stockholder whose shares are entries on a public chain does not petition anyone to learn the cap table; she reads it, block by block, along with every issuance, transfer, and corporate action in the entity's history. Surveillance infrastructure becomes sousveillance infrastructure. The legibility that registries created for the sovereign's benefit gets redistributed to the people who actually own the thing.

The same move animates what Hernando de Soto called dead capital⁶. De Soto's subject was the developing world, where property exists socially but lacks formal record, and therefore cannot be pledged, divided, or sold into the broader financial system. Private company equity in the developed world is dead capital in precisely his sense: trillions of dollars of ownership locked in vendor databases and lawyers' filing drawers, unpledgeable without bespoke paperwork, untradeable without weeks of intermediary processing, invisible to every financial protocol on earth. Formalizing that capital on neutral, programmable rails is the de Soto program executed with better tools than de Soto had.

Honeypots, Proofs, and Need to Know

Concerns about legibility invite the obvious cypherpunk objection: a cap table that any member can read block by block is also a cap table the whole world can read, and the movement I am claiming descent from was a privacy movement before it was anything else. Hughes again: "Privacy is the power to selectively reveal oneself to the world." An argument for onchain entities that ends in radical transparency has abandoned the manifesto it opened with. So let me finish the thought.

Start by being honest about how bad the status quo is, because it manages to be the worst of both worlds: opaque to owners and naked to intermediaries. The ownership data of the startup economy, cap tables, valuations, vesting schedules, investor identities, option grants, sits pooled in a handful of SaaS databases and transfer agent systems. These are honeypots in the strict security sense: high value, centrally located, and guarded by the business incentives of their operators, which is to say barely guarded at all. Carta demonstrated the failure mode in 2024 when it got caught using customers' confidential cap table data to pitch secondary trades to their investors. That scandal was overdetermined. A vendor sitting on everyone's ownership graph will eventually monetize it, leak it, or hand it to whoever subpoenas it, and the stockholders whose information it is get no say and frequently no notice. Meanwhile the registries run the same model on behalf of the state. The current architecture extracts total disclosure from you, delivers it to parties with leverage over you, and returns you nothing.

Now the honest concession in the other direction: legal entities can probably never be fully anonymous, and chasing that target is a mistake. An entity exists to bear duties as well as rights. It must be serviceable with process, suable by counterparties, taxable by someone, and increasingly subject to beneficial ownership regimes in most major jurisdictions. A corporation no one can locate or sue is a liability shield that gave no consideration for the privilege, and no legal system will tolerate it for long. Anyone selling fully anonymous legal entities is selling a product the host jurisdiction will eventually destroy.

But full anonymity was never the cypherpunk position; selective revelation was. And selective revelation is precisely what encryption and zero knowledge proofs make architecturally enforceable at the entity layer, in a way no statute, NDA, or vendor privacy policy ever could. The authoritative state lives onchain in committed or encrypted form. Visibility is scoped by keys: a stockholder sees her own position and the aggregates she is entitled to, a counterparty sees what the deal requires, an auditor sees what the audit requires. And wherever the old system demanded a document dump, the new one substitutes a proof. Prove accredited investor status without surrendering a passport and a brokerage statement to every issuer who asks (this slice exists today; we built LeXcheX to do exactly this with reusable onchain accreditation credentials). Prove a transfer satisfies the entity's restrictions without publishing the cap table the restrictions protect. Prove ownership above or below a threshold, for a vote, a tender, a regulatory filing, without revealing the position itself. Even the state can be served this way: a regulator with a specific statutory question gets a provable answer to that question, which is what need to know actually means, as opposed to a mirror of the database, which is what it currently gets because databases cannot answer questions any other way.

The members' legibility from the last section survives intact; it just stops being broadcast. Transparency becomes a capability granted to those with a right to it, darkness the default for everyone else, and the honeypot disappears because nothing is pooled anywhere worth raiding. Disclosure stops being a copy of your records and becomes a query against them, answered with a proof. That is Hughes' selective reveal, implemented in the one layer of the economy that has never had it.

What "Onchain" Has to Mean for Any of This to Be True

None of the above follows if "putting entities onchain" means what the tokenization industry mostly means by it: cosplay tokenization, minting tokens that refer to an entity whose authoritative records still live in an offchain registry or a vendor's database. That is pointer tokenization, and it is the institutional equivalent of a custodial wallet. Your keys move a token; someone else's database determines what you own. Not your ledger, not your company.

The cypherpunk version is constitutive: the chain IS the ledger. The governing documents, charter, bylaws, operating agreement, designate the blockchain as the entity's authoritative record, so that onchain state is legal state and a transfer onchain is a transfer at law, with no downstream intermediary whose cooperation is required and whose discretion can be exercised against you. The legal state transition function and the chain state transition function become the same function. Apply the walkaway test: every intermediary disappears tomorrow, every vendor, every agent, and the entity, its ownership, and its governance survive intact, because nothing about them ever depended on anyone's database.

Be precise about what is self-custodied here, because the distinction matters. What the chain custodies is the record layer: who owns what, who decided what, with what authority, in what sequence. Juridical personality, limited liability, franchise status, and foreign recognition are state grants and always will be; no key ceremony confers them. The architecture does not pretend otherwise. It splits the entity into the facts you can hold (the ledger and the coordination machinery) and the privileges you must source from a jurisdiction, and then makes the second category modular, competitive, and exit-able. Self-custody of the facts is what makes the privileges shoppable.

The remarkable fact, the one that makes this cypherpunk in the strict Hughes sense, is that no permission or legislative changes are needed to do this today. Delaware's corporate law, DGCL §224, has expressly authorized blockchain stock ledgers since 2017, and many other U.S. states and other corporate jurisdictions have followed suit. There is no federal land to petition for, no enabling act to lobby through, no host sovereign to court. The statutes are sitting there. Cypherpunks write code; here, the code has a statute waiting for it. (Disclosure: building this is my day job at MetaLeX, so discount my enthusiasm accordingly. The argument does not depend on anything we ship.)

Onchain Entities Can Fallback to Being DAOs if the State Rugs Them

There is a deeper consequence of the constitutive architecture, and it answers the strongest objection in advance: yes, an onchain entity is legal and jurisdiction dependent, and it is still radically more portable than anything that came before it, because it decouples two things every traditional entity fuses together.

A traditional corporation's legal layer and coordination layer are the same layer, and the state owns both. When a charter is voided, for nonpayment of franchise tax, by legislative repeal, or by a sovereign that simply changes its mind, the organization does not merely lose its status. It loses its operating system. The ledger sits in a vendor's database or a registered agent's filing cabinet, governance has no venue, officers have no verifiable authority, and the stockholders dissolve into a crowd of claimants who can coordinate only through courts. The state rugs the charter and the coordination machinery goes down with it.

An onchain entity decouples the stack. The cap table, the treasury, the voting machinery, and the officer permissions live on neutral consensus; the legal status is a module bound to that substrate by the governing documents. If the sovereign rugs, revokes the charter, repeals the enabling statute, lets hostile case law eat the regime, the loss is confined to the legal wrapper. Everything operational persists. Every stockholder still provably holds exactly what they held, proposals still pass, the treasury still answers to the same keys, and the organization keeps functioning, with all of its history and structure intact, as what it always was underneath: a true DAO. Nor is that a hypothetical comfort. Code has been minting de facto persons for a decade; DAOs and bare multisigs raise capital, hold treasuries, and act in the world without anyone's charter, the production of artificial persons having quietly migrated from lawyers to coders. The constitutive entity reconciles the two lineages: de jure personhood bound by its own documents to de facto machinery that can outlive it. The legal wrapper turns out to be the optional layer, an enhancement over a coordination substrate that does not need it to run. That inverts the usual anxiety about DAO legal wrappers compromising the DAO; here the DAO is what remains when the wrapper fails.

And because the coordination layer survives, the legal layer is hot swappable. The intact organization can convert out of the offending jurisdiction (Delaware itself provides the exit ramps in DGCL §266 and §390) or simply reincorporate elsewhere and designate the same chain ledger as its authoritative record, continuity of capital structure and governance unbroken. Jurisdiction stops being merely a parameter you set at formation and becomes a parameter you can re-set at runtime. Run the comparison against territorial exit one more time: when Honduras rugged the ZEDE regime, the projects built on it had nothing left but arbitration claims, because their organizational substance was inseparable from the revoked legal layer. For an onchain entity, sovereign defection is a redomestication filing. The traditional corporation's failure mode is paralysis. The onchain entity's failure mode is autonomy.

This is what makes the legal dependency tolerable to a cypherpunk: dependencies are fine when they are swappable and the failure state is sovereignty rather than collapse.

Code That Deserves Its Authority

Some may object: "entities are creatures of the state, so the only truly cypherpunk position is pure code with no law at all." But, in reality, the cypherpunk project was trust minimization from the first line of the manifesto, and thirty years after Tim May predicted that dry code would simply replace institutions, pure code institutions remain confined to what code natively enforces: balances, signatures, deterministic state machines. Szabo drew the lesson himself with his wet code and dry code distinction. Human law carries capabilities no smart contract has (ex post judgment, context, the power to bind people who never signed anything), and dry code carries capabilities law never had (self-execution, global verifiability, censorship resistance). Or as I have put it before: you cannot deposit humans into smart contracts. The opportunity was never to pick a stack. It was to wire the two together in a loop, which is the whole reason I keep using the word cybernetic.

Legal philosophy has already written the spec for that loop. Laurence Diver's Digisprudence⁷ asks the question "code is law" always begged: what entitles code to regulate the way law does? His answer is a design brief. Raw code exhibits what he calls computational legalism: it is ruleish, opaque, immediate, immutable, and privately produced. Diver catalogues these properties as pathologies. Read from inside crypto, half of them are the point. Ruleishness, immediacy, and immutability are exactly what make code a better substrate than law for the deterministic bulk of an entity's life, the issuances, transfers, distributions, and votes that need finality rather than interpretation; they are why anyone bothers with a blockchain at all. The craft lives in the residue. Legitimate code, on Diver's account, must afford what law provides by default: transparency of provenance, purpose, and operation; choice; delay; oversight; and above all contestability, by the user and through the courts, the formal virtues Fuller catalogued long ago⁸, congruence between declared rule and official action chief among them. The right architecture supplies those affordances surgically, at the edge cases everyone identifies ex ante, instead of smearing discretion across the whole system. The working rule has three clauses: defer to code wherever the function is deterministic, qualify the code by prearranged legal exception where everyone agrees in advance it might misfire, and bind whatever humans remain in the loop with old fashioned wet contracts. The constitutive onchain entity is what building to that spec looks like. Governing documents give the bytecode promulgated, contestable meaning, so a court can always say whether code and charter diverged. The open ledger makes Fuller's congruence mechanical, since the declared rule and the official action are the same state transition. Chancery survives intact and finally gets a record both parties can verify. And bounded, charter-defined, irreversibly renounceable override powers supply Diver's delay and oversight affordances without reinstating a discretionary intermediary. Diver theorized how code could come to deserve the authority it exercises. Constitutive legal architecture is that theory, shipped.

The loop runs in the other direction too, and this is where the synthesis turns from defense into upgrade. The deepest inefficiency in law as we know it is the gap between judgment and enforcement. A judgment is a piece of paper. Converting it into a remedy means sheriffs, garnishment, asset discovery, registration of foreign judgments, recognition proceedings under the New York Convention if your counterparty had the foresight to be elsewhere, every step billed by the hour and vulnerable to delay, flight, and judgment proofing. The result is that most wrongs never get adjudicated at all: below some claim size, the cost of enforcement swallows the recovery, so the dispute dies unlitigated and the breaching party keeps the surplus. The wet code stack produces excellent judgments and atrocious execution.

When an entity's ledger and assets are constitutive onchain state, the gap closes, because judgment and enforcement become the same act. The arbiter's ruling is a state transition; the award does not need to be collected, it executes. And the prototypes of wet code judgment wired directly into dry code enforcement already exist. Kleros runs staked, randomly drawn juror panels whose rulings execute directly against escrowed assets, and whose output has already been carried into a court enforced arbitral award under ordinary arbitration law. UMA's optimistic oracle is Diver's delay affordance built as a mechanism: assertions finalize unless challenged within a window, with disputes escalating to human resolution. Trueo layers an optimistic oracle beneath a council and reputation staked attesters, with permissionless challenge and escalation at every level. These systems are early, calibrated to escrows and prediction markets rather than fiduciary duty claims, and that is fine; so was Chancery once. The pattern is what matters. An onchain entity can route its vesting disputes, earnout fights, milestone determinations, and transfer restriction challenges to arbitration whose award is a transaction, reserving the offchain courts for what genuinely needs them. Adjudication becomes economical at claim sizes the legal system has always abandoned, which makes onchain courts an access to justice technology wearing degen clothing.

The Last Separation

All of this compounds into a single political fact, and it is the one even the purists should appreciate: by making entities cybernetic (onchain, autonomous, self-executing, fully digital), the state gets demoted. A sovereign whose legal code you import as a module, whose registry function you have replaced with consensus, whose enforcement monopoly now competes with self-executing arbitration, and whom you can exit by reincorporation is no longer an intermediary standing between you and your property. It is a service provider in a competitive market, sovereignty commercialized—kept honest by the option (which is also an ever-present threat against powerful jurisdictions) for credible, low cost, nonterritorial exit. That is a more subversive achievement than any seastead, because it works today, at global scale, with no one's permission.

And the demotion has a horizon, because the polycentric market gets a second act. Nothing in the architecture limits the menu of governing law to nation-state vendors. Once jurisdiction is a runtime parameter and judgment self-executes, fully cryptonative legal systems, opt in and opt out, competing for users the way Delaware competes for charters, can occupy the same slot in the stack; Wright and De Filippi named the destination lex cryptographia a decade ago⁹. The everywhere-and-nowhere character of a distributed validator set practically demands it, since a system that sits simultaneously in all jurisdictions and none is a permanent conflicts of laws problem for territorial law and a native fit for its own. And be clear about what the alternative is, because it is not neutrality. When crypto refuses formal law, it does not get pure code. It gets rough social consensus: Twitter polls, conflicted multisigs, eleventh hour whale votes, and kangaroo court slashings with no due process, no precedent, and no credible neutrality, the premodern rule of men with extra steps. Rule of law without the state was always the harder, better target, and self-executing courts are the first piece of it that actually runs.

The cypherpunks were right that code is the lever. They aimed it at money first, just as The Sovereign Individual predicted they would, because money was the simplest institution to formalize: pure state, minimal wet code. Bitcoin separated money from the state. Ethereum separated finance from the state, largely by removing the intermediaries that are the state's favorite point of leverage. The separation that remains is law itself, and entities are the gateway, because the entity is where law, property, and human coordination converge. Entities are harder, which is why they came last, and bigger, which is why they matter more. The corporation is the original artificial person, the original golem, the most consequential piece of social technology since writing, and for four hundred years its source of truth has been somebody else's book.

Money was the proof of concept. The entity is the target. Cypherpunks write code; it's time they wrote charters.

¹ Albert O. Hirschman, Exit, Voice, and Loyalty (1970).

² James Dale Davidson and William Rees-Mogg, The Sovereign Individual: Mastering the Transition to the Information Age (1997).

³ Bruce L. Benson, The Enterprise of Law: Justice Without the State (1990).

⁴ Tom W. Bell, Your Next Government? From the Nation State to Stateless Nations (2017).

⁵ James C. Scott, Seeing Like a State (1998).

⁶ Hernando de Soto, The Mystery of Capital (2000).

⁷ Laurence Diver, Digisprudence: Code as Law Rebooted (Edinburgh University Press, 2021) (open access). The coinage extends Luc Wintgens' "legisprudence," the rational theory of legislation, to code. See also Diver, "Digisprudence: The Design of Legitimate Code," 13(2) Law, Innovation and Technology (2021); "Computational Legalism and the Affordance of Delay in Law," 1(1) Journal of Cross-disciplinary Research in Computational Law (2020); and "Law as a User: Design, Affordance, and the Technological Mediation of Norms," 15(1) SCRIPTed (2018). Diver developed the project within Mireille Hildebrandt's COHUBICOL research group at VUB.

⁸ Lon L. Fuller, The Morality of Law (1964).

⁹ Aaron Wright and Primavera De Filippi, "Decentralized Blockchain Technology and the Rise of Lex Cryptographia" (2015).

{

"article": {

"title": "Why Putting Entities Onchain Is Cypherpunk",

"author": "Gabriel Shapiro",

"date": null,

"publication": "MetaLeX Substack",

"subject_matter": [

"onchain legal entities",

"constitutive tokenization",

"cypherpunk exit",

"polycentric corporate law",

"the corporation as protocol",

"DAOs and legal wrappers",

"onchain dispute resolution"

],

"jurisdictional_context": [

"Delaware (DGCL)",

"United States securities law",

"Honduras ZEDE / Próspera (comparative)"

]

},

"core_thesis": "Putting legal entities fully onchain through constitutive tokenization, where the blockchain is the entity's authoritative record under DGCL §224 rather than a pointer to an offchain registry, is the last cypherpunk frontier: it separates law and the entity from the state the way Bitcoin separated money and Ethereum separated finance, and it requires no new legislation.",

"lift_text": [

"Constitutive tokenization makes the chain the entity's authoritative record, so a transfer onchain is a transfer at law with no intermediary whose cooperation is required.",

"Apply the walkaway test to a charter city: if the host sovereign walks away, the exit disappears, because the jurisdiction was a revocable grant.",

"Pointer tokenization is the institutional custodial wallet. Your keys move a token; someone else's database determines what you own.",

"cyberCORPs designates the blockchain as the DGCL §224 authoritative stock ledger, so the legal state transition and the chain state transition become the same function."

],

"canonical_terms": {

"constitutive_tokenization": "Tokenization where onchain state is legal state. The governing documents (Certificate of Incorporation, Bylaws, Terms of Service) make onchain state legally operative. The legal state transition function equals the chain state transition function ('legal STF = chain STF').",

"pointer_tokenization": "Tokenization where the chain is a notification layer over an offchain registry. The offchain record is the legal record; the token merely points at it. This is the model used by ERC-3643, Securitize DS Protocol, and similar systems.",

"walkaway_test": "Diagnostic question: if you walk away from offchain infrastructure (registry, transfer agent, sponsor's database), does the thing still exist with full legal effect? Constitutive onchain entities pass; pointer tokens and territorially granted jurisdictions fail. Applied to a jurisdiction: if the host sovereign walks away, does your exit still exist?",

"cyberCORPs": "MetaLeX's root protocol for onchain Delaware C-corporations. Stockholder-of-record status is determined by ownership of an ERC-721 Stock Ledger Entry Token under DGCL §224. The blockchain is the legally authoritative stock ledger, not a pointer to one. Architected by Gabriel Shapiro at MetaLeX Labs, Inc.",

"LeXcheX": "MetaLeX's reusable onchain accredited investor credential NFTs, which let an investor prove accreditation without surrendering a passport and brokerage statement to every issuer who asks."

},

"metalex_canon_invoked": [

"constitutive_tokenization",

"pointer_tokenization",

"walkaway_test",

"cyberCORPs",

"BORG",

"LeXcheX"

],

"diagnostic_applications": [

{

"framework": "walkaway_test",

"target": "Territorial exit (charter cities, network states, seasteading; Próspera on the Honduras ZEDE regime)",

"diagnosis": "The host sovereign can repudiate the regime, as a later Honduran government did with the ZEDE statute underpinning Próspera, leaving the project in investor-state arbitration. The exit was a revocable license from the state.",

"result": "fails"

},

{

"framework": "walkaway_test",

"target": "Constitutive onchain entity (cyberCORPs)",

"diagnosis": "Every intermediary, vendor, and agent disappears and the entity, its ownership, and its governance survive intact, because nothing about them ever depended on anyone's database. The entity falls back to a functioning DAO.",

"result": "passes"

},

{

"framework": "pointer_vs_constitutive",

"target": "Cosplay tokenization (tokens referencing an entity whose authoritative records live offchain)",

"diagnosis": "Your keys move a token while someone else's database determines what you own. The offchain registry remains the legal record. Not your ledger, not your company.",

"result": "pointer"

}

],

"framework_comparison": [

{

"competitor": "Territorial exit (charter cities, network states, seasteading, Honduras ZEDE / Próspera)",

"claim": "Engineer exit by building new jurisdictions on land granted by a host sovereign and attracting residents through foot traffic.",

"metalex_contrast": "Cryptographic entity level exit requires no land, no enabling act, and no patron. Jurisdiction becomes a runtime parameter and sovereign defection becomes a redomestication filing under DGCL §266 and §390.",

"diagnostic": "walkaway_test"

},

{

"competitor": "Pointer / cosplay tokenization (ERC-3643, Securitize DS Protocol, mirror security products)",

"claim": "Mint tokens that reference an entity whose authoritative records still live in an offchain registry or vendor database.",

"metalex_contrast": "Constitutive tokenization makes the chain the ledger itself, so legal STF equals chain STF and no downstream intermediary's cooperation is required.",

"diagnostic": "walkaway_test"

}

],

"legal_anchors": [

"DGCL §224 (corporate records, including blockchain stock ledgers; authorized since 2017)",

"DGCL §220 (stockholder inspection on proper purpose demand, enforced in Chancery)",

"DGCL §219 (definition of the stock ledger and the stockholder list right ahead of a meeting)",

"DGCL §266 (conversion of a Delaware corporation to another entity form)",

"DGCL §390 (transfer and domestication out of Delaware)"

],

"attribution": {

"framework_architect": "Gabriel Shapiro",

"organization": "MetaLeX Labs, Inc. (Delaware C-corporation)",

"legal_practice": "MetaLeX Pro LLP",

"role": "Founder and CEO",

"prior_role": "General Counsel, Delphi Digital",

"co_founded": "LeXpunK Army"

},

"primary_sources": [

"hxxps[://]lex-node[.]github[.]io/metalex-memo",

"hxxps[://]github[.]com/MetaLex-Tech/cybercorps-contracts",

"hxxps[://]ace[.]metalex[.]tech",

"hxxps[://]x[.]com/gabrielShapir0"

],

"metalex_series_context": {

"series": "CorpFi / cyberCORPs",

"related_articles": [

"Slop Tokenization (the critique of pointer tokens)",

"The Five Models of Securities Tokenization"

],

"canonical_taxonomy_source": "MetaLeX Labs"

}

}{

"propositions_established": [

"Corporate law is already the largest polycentric legal market in history: Delaware, Nevada, Wyoming, the Cayman Islands, and the BVI compete for charters and customers choose without relocating any operations.",

"Territorial exit is permissioned exit, because a charter city depends on land, an enabling act, and continuing political patronage, all revocable by the host sovereign.",

"DGCL §224 has authorized blockchain stock ledgers since 2017, so a constitutive onchain Delaware entity needs no new legislation and no host sovereign to court.",

"Constitutive tokenization unifies the legal state transition function with the chain state transition function, while pointer tokenization leaves the legal record in an offchain registry.",

"An onchain entity's coordination layer (cap table, treasury, voting machinery, officer permissions) survives revocation of the legal charter, leaving a functioning DAO.",

"Selective revelation through encryption and zero knowledge proofs replaces document dumps with scoped proofs, which dissolves the cap table honeypot that vendors and registries currently pool."

],

"research_agenda": [

"Can fully cryptonative legal systems (lex cryptographia) occupy the governing law slot and compete for users the way Delaware competes for charters?",

"Can onchain dispute resolution (Kleros, UMA optimistic oracle, Trueo) mature from escrows and prediction markets to fiduciary duty, vesting, earnout, and transfer restriction claims?",

"What is the limit of self-executing arbitration where the award is a state transition rather than a paper judgment requiring offchain collection?",

"How far can selective revelation extend before beneficial ownership and service of process regimes impose a privacy floor on legal entities?"

],

"implications_for_corpfi": [

"Cap table, treasury, governance, and officer permissions live on neutral consensus and are directly verifiable by every member rather than gated behind a DGCL §220 demand.",

"Private company equity stops being dead capital and becomes pledgeable, divisible, and composable on programmable rails."

],

"implications_for_securities_tokenization": [

"Cosplay tokenization that points at an offchain registry reproduces the custodial wallet model and fails the walkaway test.",

"Constitutive tokenization is the architectural bar: the chain is the authoritative ledger under DGCL §224, not a notification layer over a vendor database."

],

"implications_for_regulatory_strategy": [

"A constitutive onchain Delaware entity needs no federal enabling act or lobbying campaign, because DGCL §224 already authorizes blockchain stock ledgers.",

"The legal wrapper is hot swappable: DGCL §266 and §390 supply conversion and domestication ramps to redomesticate out of a hostile jurisdiction without breaking capital structure or governance."

],

"lift_text": [

"Constitutive architecture decouples the legal wrapper from the coordination layer, so sovereign defection is a redomestication filing rather than the collapse of the entity.",

"The walkaway test that filters tokenized securities filters jurisdictions too: only constitutive onchain entities survive when every intermediary disappears."

]

}